Many high-income professionals accumulate significant savings inside traditional retirement accounts. Those accounts grow tax-deferred, but withdrawals in retirement are generally taxed as ordinary income.

A Roth conversion moves assets from a traditional retirement account into a Roth account, where future qualified growth is never taxed again.

The conversion occurs after investing retirement funds into a private investment and obtaining an independent valuation of that investment.

The objective is to complete the conversion based on the investment’s fair market value at the time of conversion, rather than the original capital invested.

How the Strategy Works

A simplified version of the process may look like this:

- Invest retirement funds from a self-directed traditional IRA or similar account into a private investment, such as a real estate syndication.

- After the investment is established, an independent valuation professional determines the fair market value of the ownership interest.

- Because the investment is a minority interest in a private, illiquid asset, the fair market value may differ from the original capital invested.

- The investor converts the investment from the traditional account to a self-directed Roth IRA.

- Taxes are owed on the fair market value at the time of conversion, not on future growth.

If the investment performs well, future appreciation inside the Roth account may occur tax-free, assuming Roth rules are satisfied.

In simple terms, the investor is paying tax on the value today rather than on potential future growth.

Why High-Income Physicians Pay Attention

For many physicians and other high-income professionals, taxes represent one of the largest lifetime expenses.

Traditional retirement accounts provide tax deferral, but distributions later in life are generally taxed as ordinary income.

A Roth conversion changes the structure of the account:

- The converted amount is taxed today.

- Future qualified growth is never taxed again.

Why the Valuation May Differ From the Initial Investment

Private investments often do not have a readily observable market price. Because of that, valuations rely on established fair market value methodologies.

In some cases, the value of a minority ownership interest in a private investment may differ from the initial capital contribution due to factors such as:

- Lack of control over the underlying asset

- Limited marketability of the ownership interest

- Illiquidity and absence of a public market

- Early-stage project risk

These valuation principles are widely used in business valuation, estate planning, and private market investing.

The key requirement is that the value used for a Roth conversion must represent a defensible fair market value determined using accepted professional standards.

A Simple Illustration

Example:

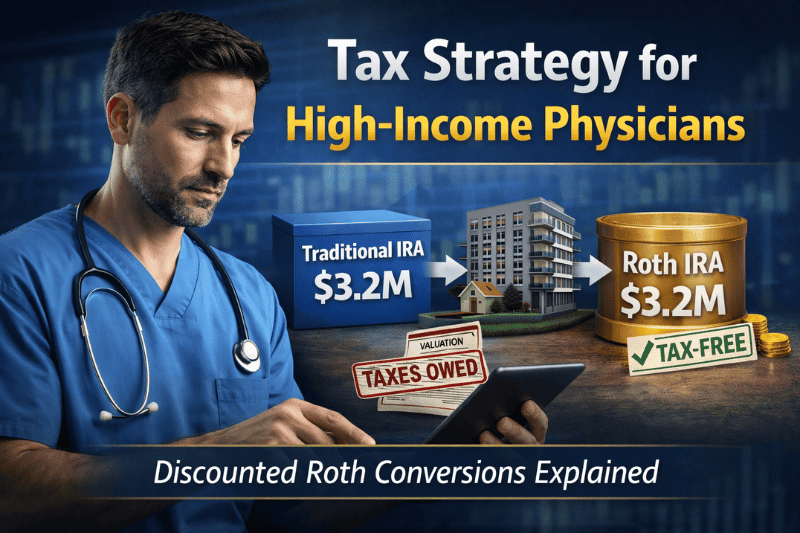

An investor places $100,000 from a self-directed retirement account into a private real estate syndication.

An independent valuation later determines that the fair market value of the ownership interest is $50,000.

If the investor converts that interest to a Roth IRA while in a 37% tax bracket, the federal tax owed on the conversion would be approximately:

$50,000 × 37% = $18,500

If investments inside the Roth compound grow successfully over time, the account value could grow significantly. For illustration, if multiple successful investments compounded to $3.2 million inside the Roth, qualified withdrawals would generally not be taxed.

If the same growth occurred inside a traditional IRA, future distributions would typically be taxed as ordinary income. Depending on tax brackets and state residency at retirement, that could materially reduce the amount ultimately kept.

Timing Considerations

Valuations are typically performed after the investment is established and capital has been deployed, but before significant appreciation has occurred.

The purpose is not to create an artificial discount, but to determine the fair market value of the ownership interest at that specific point in time.

If the investment has already appreciated meaningfully, the valuation used for the Roth conversion may be higher.

Common Questions

Is there an income limit to convert?

No. Income limits apply to Roth contributions, but not to Roth conversions.

Is there a cap on how much you can convert?

There is no dollar limit on Roth conversions. The tax owed depends on the amount converted and your tax bracket.

Do you need a self-directed Roth?

Typically yes. Private investments such as syndications generally require a self-directed custodian because traditional brokerage Roth accounts usually do not allow these types of assets. If you do not have a self-directed account, we can help you set one up.

When is the tax due?

Conversion income is generally included in taxable income for the year of the conversion. Taxes are usually due by the following tax filing deadline, although estimated payments may apply.

Costs, Risks, and Important Considerations

Independent valuations typically involve professional fees. Cost typically run $1200-$1400 depending on the complexity of the asset.

Valuations rely on professional judgment and accepted methodologies. The IRS has the authority to review or challenge a valuation.

Private investments also carry risk, including the possibility of loss of principal.

Want to See If This Strategy Fits Your Plan?

If you would like to explore whether a Roth conversion involving private investments may fit your broader plan, you can schedule a conversation with our team.

We can review how self-directed accounts work, discuss how private investments fit within retirement structures, and help you understand the next steps to discuss with your tax and financial advisors.

👉 Schedule a call with Timberview Capital to learn more

https://timberviewcapital.com/schedule/