Small Business Accounts Receivable Fund

This investment has the advantages of strong monthly cash flow and liquidity.

The Small Business Receivables Fund offers qualified investors access to a consistent income stream by participating in the purchase of short-term receivables from established small businesses across the United States.

Rather than traditional loans, this fund advances capital to small businesses in return for their accounts receivable, which are repaid daily or weekly, allowing for fast capital recycling and monthly distributions to investors.

Small Business Accounts Receivable Fund

This investment has the advantages of strong monthly cash flow and liquidity.

The Small Business Receivables Fund offers qualified investors access to a consistent income stream by participating in the purchase of short-term receivables from established small businesses across the United States.

Rather than traditional loans, this fund provides revenue-based advances giving business owners the working capital they need in exchange for a portion of their future revenue. These receivables are repaid daily or weekly, allowing for fast capital recycling and monthly distributions to investors.

Targeted Preferred Returns

| Investment Range | Preferred Return |

|---|---|

| $100K | 11% |

| $200K | 12% |

*Distributions are paid monthly.

Targeted Preferred Returns

| Investment Range | Preferred Return |

|---|---|

| $100K | 11% |

| $200K | 12% |

*Distributions are paid monthly.

Key Investment Details

- Minimum Investment: $100,000

- Preferred Return: 11–12%, based on commitment

- Distributions: Monthly (after first full month active)

- Liquidity: 12-month lock-up, then 90-day notice period to recall capital

- Structure: True sale of future receivables (not loans)

- Capital Protection: Portfolio stress-tested to withstand 25%+ defaults

- Historical Default Rate: Just 4–6% annually from the origination partner

Key Investment Details

- Minimum Investment: $100,000

- Preferred Return: 11–12%, based on commitment

- Distributions: Monthly (after first full month active)

- Liquidity: 12-month lock-up, then 90-day notice period to recall capital

- Structure: True sale of future receivables (not loans)

- Capital Protection: Portfolio stress-tested to withstand 25%+ defaults

- Historical Default Rate: Just 4–6% annually from the origination partner

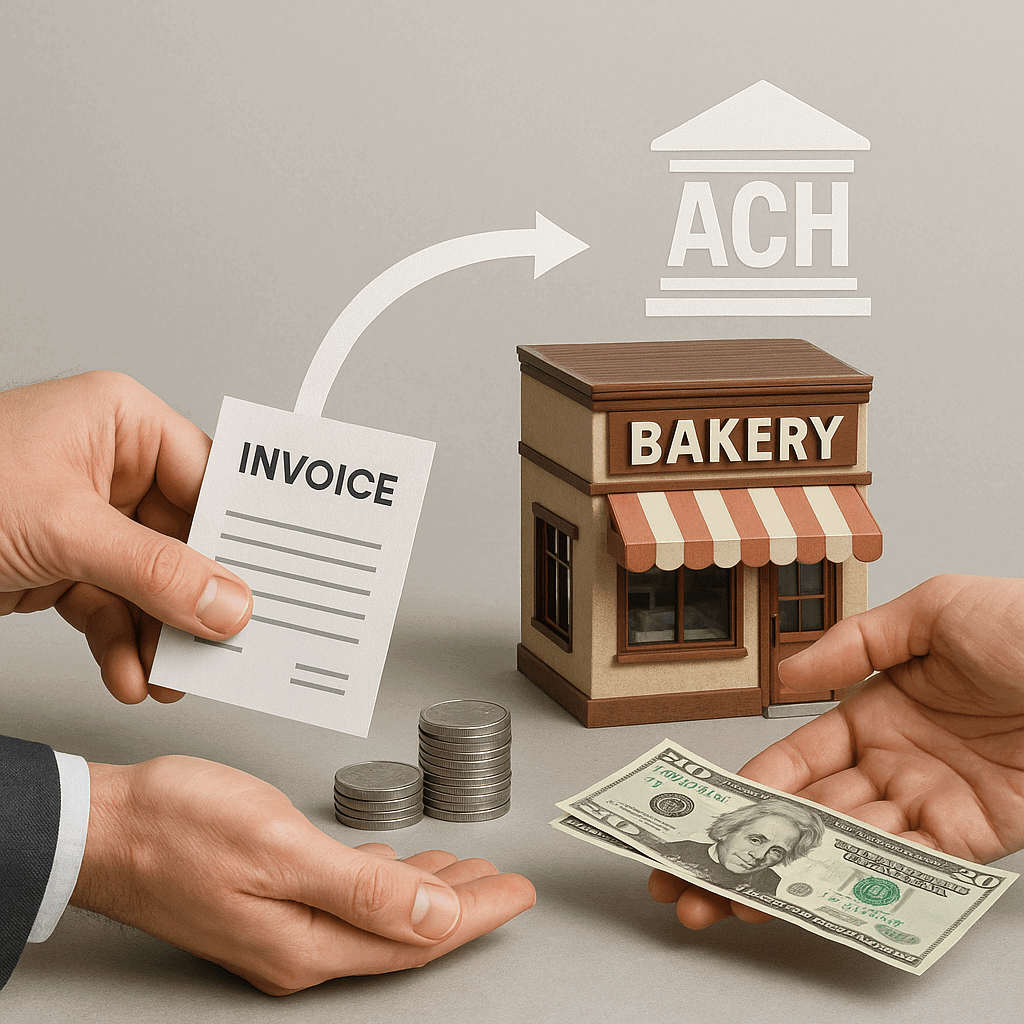

How the Strategy Works

- The fund finances U.S. businesses by purchasing short-term receivables

- Payments are collected directly from business revenue via daily or weekly ACH transfers

- Typical repayment duration: 4–12 months

- Your capital is diversified across a large portfolio with no oversized exposures

- Originated through a top-tier partner with $900M+ in funded volume and $250M projected for 2025

How the Strategy Works

- The fund finances U.S. businesses by purchasing short-term receivables

- Payments are collected directly from business revenue via daily or weekly ACH transfers

- Typical repayment duration: 4–12 months

- Your capital is diversified across a large portfolio with no oversized exposures

- Originated through a top-tier partner with $900M+ in funded volume and $250M projected for 2025

What Sets This Fund Apart

Monthly Income provides steady returns while avoiding volatility of the stock market.

High-Frequency Repayments recycle capital quickly to create steady growth for investors.

Diversified Portfolio reduces risk across regions, industries, asset classes, and sizes.

Aligned Incentives ensure sponsor is paid only after investors receive their set return.

Efficient Liquidity allows short repayment terms with 90-day redemption after lock-up.

What Sets This Fund Apart

Monthly Income provides steady returns while avoiding volatility of the stock market.

High-Frequency Repayments recycle capital quickly to create steady growth for investors.

Diversified Portfolio reduces risk across regions, industries, asset classes, and sizes.

Aligned Incentives ensure sponsor is paid only after investors receive their set return.

Efficient Liquidity allows short repayment terms with 90-day redemption after lock-up.

Frequently Asked Questions

How is the funding structured and secured?

Each transaction is structured as a true sale of future receivables—not a loan. We purchase a fixed amount of the business’s future revenue at a discount. The business repays us via daily or weekly ACH payments based on its receivables. This structure secures our position through direct access to the business’s cash flow, not collateral or personal guarantees. All opportunities go through comprehensive underwriting, with a strong emphasis on current, verifiable cash flow rather than speculative growth potential.

Who is actually receiving the funding?

Our capital is deployed to U.S.–based small and midsize businesses, often seeking working capital, inventory, or short–term growth capital. More than 50% of our deals are with returning businesses who have already repaid us in the past.

What is the typical duration of each funding?

Most positions are structured for 4 to 12 months. Payments are made daily or weekly, which means capital and return begin coming back almost immediately after deployment. This frequent repayment schedule allows us to recycle capital quickly, manage risk dynamically, and maintain consistent cash flow throughout the portfolio.

How often are investor distributions paid out?

We target monthly income distributions, sourced directly from our funding repayment streams. Distributions begin after the first full month your capital is active in the fund

What fees do you charge?

There are no fees at the manager level. Investors receive their full preferred return—11% or 12%, depending on check size—before we participate in any upside. We only earn after you’re fully paid, so our interests are 100% aligned with yours.

Why haven’t banks taken over this space?

Banks are too slow and rigid for most of our clients’ needs. Our businesses often need funding in 24–48 hours, and we deliver with underwriting that banks can’t match in speed or flexibility. We’re built to serve time–sensitive capital needs—making us the preferred partner for thousands of growing businesses.

How do you vet funding opportunities?

We’ve completed close to $1 billion in total transactions and maintain a proprietary database of over 10,000 businesses. This historical data gives us deep insight into repayment behavior by industry, geography, and size. Each opportunity is evaluated against these real–world patterns—so our decisions

are driven by what’s proven to work, not theory.

What are typical use cases for the funding?

Examples include: Seasonal inventory purchases, emergency payroll or short–term cash flow gaps, bridge capital while awaiting SBA or bank loans, expansion, equipment, or growth–related working capital. These are real–time needs that traditional lenders can’t respond to quickly enough.

What is the typical size of each funding?

Most individual fundings range from $25,000 to $250,000. We may selectively consider larger positions but only when the portfolio is sufficiently diversified and no single funding creates excessive exposure. Our risk management framework ensures that no individual deal can meaningfully disrupt overall performance.

What happens if a business stops paying?

Our structure is designed to protect investors well before full repayment is due. Since we collect frequent, scheduled payments, we typically recover a meaningful portion of principal and return before any disruption occurs. We also maintain full servicing of the business relationship, giving us direct control to identify issues early and find solutions—such as temporary payment adjustments or structured resolutions. This active, relationship–driven approach helps us keep recovery efforts efficient and capital protected.

How liquid is this investment?

There is a 12–month lockup on invested capital. After that, investors may request redemptions with 90 days’ notice. Because of our short–term duration and recurring payment model, we expect strong liquidity—but include this notice period to protect fund performance and investor experience.

What downside protection do investors have?

Our model is built to withstand defaults and volatility. Investor returns are protected unless 25%+ of fundings default with zero recovery. Investor principal is not at risk unless defaults exceed 30%+ of the total portfolio. Historically, defaults on fundings brokered through Direct Funding Now—our proprietary origination partner—have averaged just 4–6% per year. By combining frequent repayment, broad diversification, and tight underwriting, we’ve engineered the Income Fund to perform in a range of market environments.

Ready to Explore This Opportunity?

Capital accepted on a first-come, first-served basis.

Ready to Explore This Opportunity?

Capital accepted on a first-come, first-served basis.

Watch the Webinar Recordings

Watch the Webinar Recordings

The testimonials, statements, and opinions presented are applicable to the individuals listed. Results will vary and may not be representative of the experience of others. The testimonials are voluntarily provided and are not paid, nor were they provided with free products, services, or any benefits in exchange for said statements. The testimonials are representative of client experience, but the exact results and experience will be unique and individual to each client. All offers and sales of any securities will be made only to Accredited Investors, which for natural persons, are investors who meet certain minimum annual income or net worth thresholds or hold certain SEC approved certifications. Any securities that are offered, are offered in reliance on certain exemptions from the registration requirements of the Securities Act of 1933 (primarily Rule 506C of Regulation D and/or Section 4(a)(2) of the Act) and are not required to comply with specific disclosure requirements that apply to registrations under the Act. The SEC has not passed upon the merits of, or given its approval to any securities offered by Timberview Capital LLC, the terms of the offering, or the accuracy of completeness of any offering materials. Any securities that are offered by Timberview Capital LLC are subject to legal restrictions on transfer and resale and investors should not assume they will be able to resell any securities offered by Timberview Capital LLC. Investing in securities involves risk, and investors should be able to bear the loss of their investment. Any securities offered by Timberview Capital LLC are not subject to the protections of the Investment Company Act. Any performance data shared by Timberview Capital LLC represents past performance and past performance does not guarantee future results. Neither Timberview Capital LLC nor any of its funds are required by law to follow any standard methodology when calculating and representing performance data and the performance of any such funds may not be directly comparable to the performance of other private or registered funds.